To Our Investors and Friends,

The S&P 500 increased 7.0% during the month of August, continuing its technology-driven march higher. Oil increased 5.8% to end the month at over $42 a barrel. The 10-year rallied during the month to 72 bps, a 17 bp increase, while the spread between the 2- and 10-year widened to 58 bps. Growth’s dominance continued. The Russell 1000 Growth increased 10.3% in the month, helped by strong performance from mega-cap technology companies. The Russell 1000 Value gained 4.1%. In small caps, the differential between growth and value was far more modest as the Russell 2000 Growth expanded 5.9% and the Russell 2000 Value gained 5.4%.

In this investment letter, we attempt to answer the simple question: why is the market willing to pay more for leading technology companies than leading industrial companies? We decided to compare the top ten S&P 500 technology companies by market cap to the top ten S&P 500 industrial companies. In short, the market is placing a premium on near-term valuations for faster growing, more profitable businesses that are earlier in their lifecycle. In fact, the valuation premium of technology companies is double that of industrial companies, comparing 2021 estimated consensus earnings multiples (46x for tech and 22x for industrials).

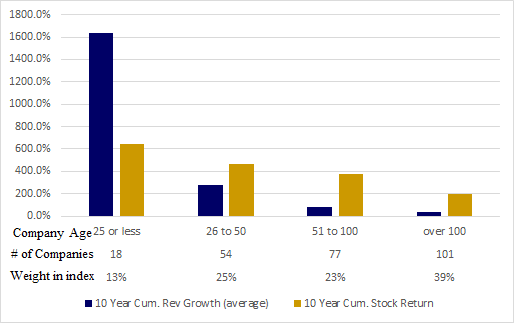

A simple examination of the fundamentals of these two groups helps explain the premium tech is receiving. Over the last 12 years, this technology cohort has grown cumulative revenue by over 1000% vs a mere 21% for the industrial cohort over the same time frame. This growth differential is entirely tied to maturity of business and global opportunity in front of them…the average tech company cohort is 28 years old addressing a global market, while the industrial cohort is 122 years old and focused on a smaller geographic footprint.

As can be seen in the chart below, the tech cohort is also far more profitable, generating 66% gross margins compared to the 32% gross margins offered by the industrial cohort. Spending on R&D and sales narrow tech operating margins to 25%, which are still higher than the mature industrial operating margins averaging 17%. This profitability advantage can be attributed to the greater scalability of tech businesses…excluding people-intensive distribution businesses Amazon (AMZN) in tech and United Parcel Services (UPS) in industrials, the average leading technology company employs less than half the number of people needed to run the industrial companies.

Fewer people required to address a larger opportunity suggests higher profitability will come to technology companies. In fact, technology companies are expected to grow earnings at more than a 40% rate over the next five years compared to a 9% rate for the leading industrial companies. Using simple math, in five years, technology companies are projected to earn approximately 5x as much as they earn today, while industrial companies are poised to earn 1.5x more. That means in five years from now, investors are paying an estimated 8.6 times for the tech earnings stream and an estimated 14.5 times for the industrial earnings stream. The market appears to have it right... tech companies are likely more undervalued than industrials if these estimates are correct. It is the FED’s “lower for longer” interest rate policy that has forced the market to appropriately place more value further out in time...a trend we expect to continue.

We will continue to search for the very best businesses the market has to offer and look to own their shares as long as their opportunities are poised to drive the growth of their businesses. Short term, the shares often appear to be rich on near-term earnings metrics, but over time, we expect them to prove their worth.

All the Best to You,

AKW