To Our Investors and Friends,

The S&P 500 increased 8.5% during the third quarter, as the bull market widened to include industrial stocks along with technology stocks on the view that earnings should accelerate as we get through the COVID crisis. Oil increased 2.4% to end the quarter at over $40 a barrel, a less robust gain on expectations for a slower demand recovery. The 10-year increased a modest 3 bps in the quarter, to .69%, while the spread between the 2- and 10-year widened 6 bps to 56 bps. Growth’s dominance continued. The Russell 1000 Growth increased 13.2% for the quarter, helped by strong performance from mega-cap technology companies. The Russell 1000 Value gained 5.6%, as financials lagged, and energy stocks plummeted. In small cap indexes, similar trends were realized as the Russell 2000 Growth expanded 7.2% and the Russell 2000 Value gained 2.6%.

This has been a year of considerable turmoil driven by the worst pandemic the world has seen in 100 years, the worst economic crisis in 90 years, and the worst social crisis since the 1960s. Possibly the greatest surprise has been the quick reversal of one of the most violent market routs in history…causing a 35% decline over a mere 23 days from mid-February to the end of March. The new bull market is being led by new leadership, which is firmly held by the fourth industrial revolution beneficiaries, those using intelligent tools to provide better solutions for their customers. Enthusiasm for these next generation businesses has spilled over into many areas, some of which are highly speculative…. especially the SPACs.

SPACs (Special Purpose Acquisition Companies) are blank check companies. Management raises money in the market with the purpose of acquiring and making public a private company. Management is incented with a large ownership stake in the SPAC, often 20%, and usually must make the investment within a predetermined time frame. Failure to make the investment, or get shareholders to approve of the investment, results in a return of capital as the SPAC is dissolved. Shareholders have the right to approve or disapprove of the investment and can sell their shares at any time, making such an investment more liquid than private equity or venture capital.

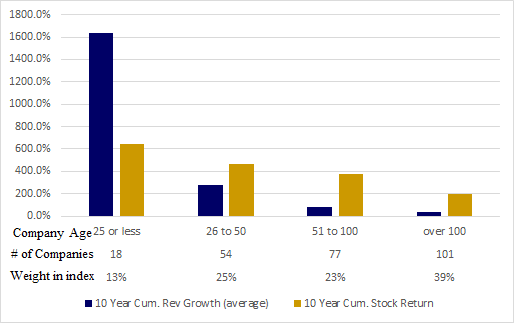

As can be seen in the Chart below, the new bull market has ushered in a speculative SPAC frenzy that has resulted in more than $80 billion in capital raised over the last year. There are now over 140 publicly traded SPACs, of which 65 became public after the market’s March bottom.

Source: William O’Neil database.

We think the SPAC craze is indicative of the public’s desire to get in on new companies early in their development. We are avoiding them, however, because they fail to meet our investment criteria. SPACs are likely the most speculative investments out there, because the SPAC investor has only a rough idea of what management intends to invest in and is completely dependent on that decision to make a return. The company that is receiving the investment is getting a very large amount of money early in its lifecycle, which heightens the prospects that bad decision-making squanders it away. This compares to venture capital investments that typically have multiple funding rounds that provide growth capital to companies over time.

We will continue to search for the very best businesses the market has to offer and look to own their shares as long as their opportunities are poised to drive the growth of their businesses. Unlike SPAC investments, these founder led businesses have been fully vetted by existing customers and public investors, dramatically reducing the chance that negative surprises present themselves like we recently witnessed with the most famous of recent SPAC investments, Nikola (NKLA).

All the Best to You,

AKW