To Our Investors and Friends,

The S&P 500 decreased 20.0% in the first quarter as the COVID-19 pandemic quickly pushed the world economy into recession. Oil prices (WTI) plummeted 66.5% to $20 a barrel as Saudi Arabia and Russia decided to meet falling demand with more supply. The 10-year collapsed 118 basis points during the quarter to end at 0.70%, while the spread between the 2- and 10-year expanded to 47 bps. Demand for treasury bonds is now only exceeded by demand for toilet paper during the current health crisis. Growth’s dominance continued even as the market plummeted. The Russell 1000 Growth fell 14.1% in the quarter, while the Russell 2000 Growth dropped a more severe 25.8%, given that smaller companies are less liquid. Value’s higher energy and financial weights caused this group to fare even worse. The Russell 1000 Value fell 26.7% and the Russell 2000 Value fell 35.7%.

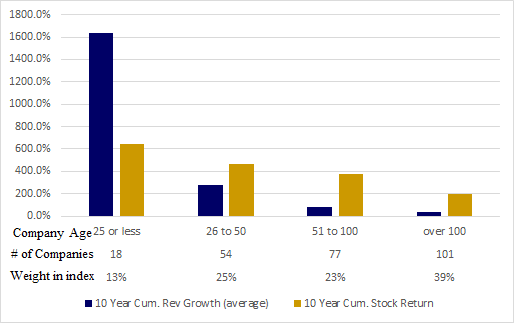

We have long held the view that industrial era businesses are slowly losing share to new companies that are more technologically savvy and less capital intensive. COVID-19 will likely act as a catalyst to an acceleration in growth of the digital economy, at the expense of the brick and mortar economy. As can be seen in the chart below, it is clear that younger businesses fared far better than older ones in the first quarter. Noteworthy, are market leaders Apple, Microsoft, and Amazon (now 26 years old) powered the 26-50 year old cohort to the best performance. The over 100 cohort was helped slightly by a number of industrial era food companies benefitting from pantry hoarding, a phenomenon we believe likely ends as the crisis abates.

Looking back at the 2008-2009 financial crisis, new leadership bottomed early, and then drove the market higher with the birth of the next bull market. Now is the time for investors to adjust their portfolios and get ready to prepare for the next bull market. It will be quite volatile at times, but will be well worth it over the long haul.

All the Best to You,

AKW